4Q21 Insights

January 24, 2022 - 5 minutes read![]()

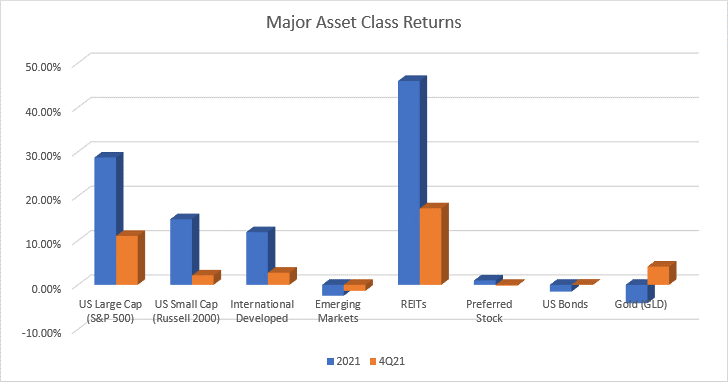

While the emergence of Omicron drove daily Covid cases to new records at the end of 4Q21, and the December inflation reading was the highest since the early 80s, the U.S. broader stock market advanced 11.0% in the fourth quarter. This brought the total return for the S&P 500 index to 28.7% for the full year of 2021.

U.S. small cap companies lagged in Q4, but still posted a 2.1% positive return.

Growth stocks outperformed value, but the performance in growth stocks narrowed significantly. With inflation running higher for longer, the fears of the Fed tightening drove many of the growth stocks down. A handful of the largest growth stocks, like Tesla (TSLA), Nvidia (NVDA), and Apple (APPL) ran up sharply in Q4 driving up the large-cap growth benchmark. On the other hand, small growth companies posted a flat quarter, ARK Innovation ETF declined 13.7%, and nearly 40% of the stocks in the Nasdaq Composite declined 50% from their 52-week highs, with almost two-thirds declining 20% or more.

International developed markets’ returns lagged U.S. but still advanced 2.7% in Q4 and 11.9% for the full year, as stronger returns in Europe, especially in France and the UK, offset weaker returns in Japan.

Emerging markets continued to struggle and posted a low-single-digit decline for the quarter and the full year, driven primarily by steep market declines in China and Brazil.

REITs continued to outperform with another 17.2% gain in Q4 and 45.9% total return for the year. This asset class has gone from worst last year to best for 2021 as the outlook for many REIT sub-sectors improved, and investors looked to real estate as potential inflation hedge.

Returns for fixed income assets, including preferred stocks and bonds, were flattish to slightly negative. Finally, gold jumped 4.1% in Q4 but was still the worst performing asset class in 2021 with 3.6% negative return, giving up some of its strong gains in prior years.

Looking into 2022, we see a somewhat mixed picture. If other countries’ experience is any guide, the Omicron variant, as menacing as the case count might imply, should peak quickly with any disruptions to the economy and supply chains being short-lived. Getting to the other side of it and treating the virus as more endemic would be a net positive for economic activity compared with last year. Consumer balance sheets are also in great shape with higher savings and spending power.

On the other hand, we see receding tailwinds from fiscal and monetary policies, as the size of government stimulus declines, and the Federal Reserve starts reducing asset purchases and hiking up interest rates.

The pace of the Fed’s tightening policy is likely to be one of the key market drivers in 2022. Typically, higher interest rates lead to lower stock valuations. This doesn’t necessarily mean that stocks decline in 2022, but a lower probability of earnings multiple expansion or even potentially contraction, earnings growth will be key for returns this year.

Current consensus for S&P 500 is for 8-9% earnings growth in 2022. While it’s not a terribly aggressive estimate, the companies will have to grow earnings in the environment where the fiscal stimulus is being pulled back, inflationary forces could pressure margins, and new legislation could increase corporate tax rates. All of this could lead to a bumpy market in the year ahead.

Geopolitical issues around Russia and China are also likely to leave an imprint in 2022, but we’d expect those to produce near-term turbulence rather than a lasting negative impact. A slowing Chinese economy and issues around the debt restructuring for its giant real estate developer Evegrande are a concern. Although that will likely lead to more accommodating fiscal and monetary policies in China.