The Importance of a Diversified Investment Portfolio

July 1, 2020 - 11 minutes readThe Importance of a Diversified Investment Portfolio

Ancient Mediterranean merchants had a saying: Ausi omnes in una nave. It meant “venture not all in one ship”. Merchants knew that putting all their goods in one ship raised the risk of loss. It was wiser to divide their goods into multiple ships or voyages. They knew it was far less likely for several ships to sink, compared to a single vessel. Allocating cargo across multiple ships mitigated their risks.

To navigate the volatile seas of today’s national and global economy, wise investors “venture not all in one ship”. Instead, they allocate investments across several financial vehicles. This practice of investment portfolio diversification can limit the impact of market volatility and reduce their risk of capital loss.

What Does it Mean to Have a Diversified Investment Portfolio?

Diversification is the practice of allocating investments among various assets and asset classes. The intent is to reduce risk and loss due to market volatility and failing ventures. Ideally, an investor will select assets that react differently to the same market or economic event.

Ever heard the saying, “Don’t put all your eggs in one basket?”

For example, during the COVID-19 pandemic, companies involved in the travel, hospitality and brick-and-mortar retail industries were negatively affected. Many companies in these sectors saw their free cash flow turn negative. As a result, suspended their dividend payments to shareholders. However, many companies in the healthcare and technology sectors did well. This is because demand soared for medical care, videoconferencing services and in-home entertainment. Several companies in these industries actually increased their dividend payments, because they had very different reactions to the same economic event.

If your investments were exclusively in the travel, hospitality and/or brick-and-mortar retail industries, the drop in stock value and the suspension of dividends might have really hurt. Conversely, if your investments were exclusively in the healthcare and/or technology sectors, the increases in stock value and dividends paid might have made you very happy. But the well-diversified investor, with investments intelligently allocated across sectors, might have enjoyed a smoother, more steady ride through the recent market volatility.

With a diversified investment portfolio, your assets do not all rise or fall at the same time.

Why You Should Have a Diversified Investment Portfolio

A diversified investment portfolio is not a guarantee against loss. But most investment professionals share the opinion that minimizing or reducing risk, via diversification, is critical to achieving long-range financial goals.

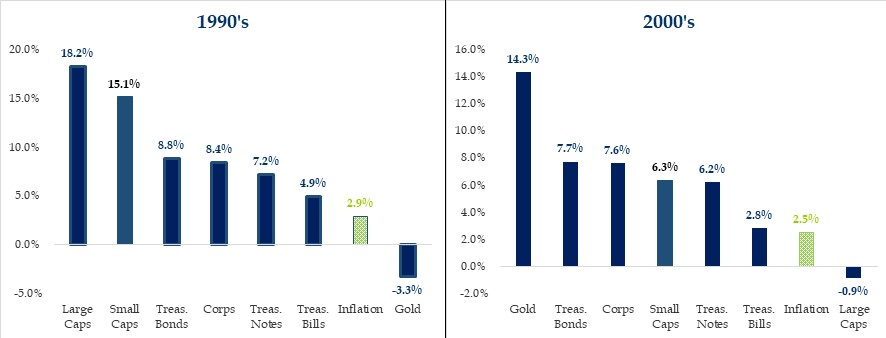

“We all like smooth and easy, but there have been days, especially earlier this year, when the stock market experienced major volatility,” remarked Bruce Rinne, a founding partner of Kunath Karren Rinne & Atkin LLC. “If that were the only asset class in your investment portfolio you probably experienced some whiplash from it all.”

“As we look back to the performance of various asset classes, we can see that some asset classes experience volatility. Some remain pretty steady, particularly bonds,” continued Rinne. “This makes an excellent argument for including the right types of bonds in a diversified investment portfolio. The bonds help to keep things steady.”

Source: Strategas Securities (Click to enlarge)

Limiting the Downside

“Protecting against big drops is the core of a diversification strategy,” said Ned Karren, a founding partner of Kunath Karren Rinne & Atkin, now retired. “With the exception of periodic down markets that can last months or even a couple of years, the stock market itself generally moves upward over time. If you are properly diversified across multiple asset classes, you may avoid those big potholes, and enjoy consistent, long-term growth. Because, if you can limit the downside, it goes a long way toward generating consistent positive returns over a 5 to 10-year period.”

“Back in 2008-2009, during that Bear market, most of our clients had a combo of stocks and bonds.” said Atkin. “After it was over, we and they talked together about how great it was to have some downside cushion. As stocks went down, bonds were either stable or went up. We’ve seen that several times over the years, where a balanced (diversified) portfolio created a lot of comfort during steep drop events in the stock market.”

Atkin also pointed out that their portfolios contained corporate bonds with maturities of five years or under and municipal bonds of seven or eight years and under. “You shouldn’t be in 30-year bonds, because they can be just as volatile as stocks,” he added.

The Primary Asset Classes

In considering the wisdom of diversifying across asset classes, it is important to identify the asset classes themselves. They are:

- Domestic Stocks

- Municipal Bonds (7-8 years or under)

- Corporate Bonds (5 years of under)

- International Stocks (individual foreign corporations and foreign ETFs)

- Commodities

- Real estate

- Gold and precious metals

While an individual asset class can suffer declines due to economic and/or political instability, it’s rare that any two or three asset classes with very different sources of risk and return would experience significant declines at the same time.

“Different assets, such as bonds and stocks, react differently to adverse events,” explained Rinne. “Generally, bond and equity markets move in opposite directions. When the economy is growing, stocks tend to outperform bonds. But when the economy slows, bonds tend to do better than stocks. By investing in both bonds and stocks, your risks are limited when there are wild swings and sudden changes in market direction.”

How Do You Properly Diversify?

Diversifying your investment portfolio goes beyond owning stocks in non-correlated industries. Intelligent diversification involves spreading your portfolio across several asset classes.

Of course, owning three non-correlated stocks is better than owning stock in one company. But ultimately, adding more and more non-correlated stocks won’t provide additional protection should the stock market decline significantly.

There are many ways to diversify your investment portfolio, but, as Rinne explains, “the primary rule should be that each investment in your portfolio should serve a different function. For instance, for stock diversification you may own several large-cap stocks, or have a S&P 500 Index fund, and also own some mid-cap and/or small-cap stocks or index funds for mid-cap and small cap. As a safety net, include some corporate or municipal bonds (depending upon your tax bracket), and as you’re able, make investments across other different asset classes, such as Real Estate or gold/precious metals. These may provide a buffer to economic shocks.”

Risk Tolerance and Portfolio Diversification

“The more time that someone has to invest, the more aggressive they could be, if they wanted to be,” explained Karren. “If their risk tolerance is high, they might want to focus on high-growth opportunities, knowing their portfolio has time to recover from a bad event.”

“But usually, as the time horizon to retirement shortens, an investor doesn’t have as much time to recover from a bad event. Generally, risk tolerance goes down as you near retirement, or when retired, and diversification may be even more important.”

“However, risk tolerance is a very relative term, a very individual thing,” he continued. “It depends on the personality of the investor, the existing assets, cash flow, time horizon and their investment goals. We’ve had investors in their 70s want their portfolios to be all stock, which is pretty aggressive. Ordinarily, investors closer to retirement, or in retirement, have a lower risk tolerance and want less stock at that time. Risk tolerance and portfolio diversification can change with time.”

“Understanding risk tolerance, time horizon, and an investor’s unique needs and goals comes from getting to know an investor as well as you can,” added Rinne. “This happens through many conversations and questions-and-answers together.”

Do you feel your investment portfolio is properly diversified?

If you are actively investing, or thinking about starting, visit with a Registered Investment Advisor. To learn more about what an Investment Advisor should do for you, click here to download our free eBook “3 Things an Investment Advisor Should Do for You”.

Anatoliy Cherevach is a Chartered Financial Analyst and a Portfolio Manager with Kunath Karren Rinne & Atkin, LLC, with over 19 years of portfolio management and security analysis experience. Prior to joining KKRA, he was a Portfolio Manager and Research Analyst with Cohen & Steers. Anatoliy holds an MBA in finance from Pacific Lutheran University. He is an active member of the CFA Institute and CFA Society Seattle.